Once the roof is in place it begins to lose its value.

New roof depreciation life.

Since the roof is newer than the structure itself the roof will technically lose its value after the building.

The difference is depreciation.

The irs states that a new roof will depreciate over the course of 27 5 years for residential buildings and over the course of 39 years for commercial buildings.

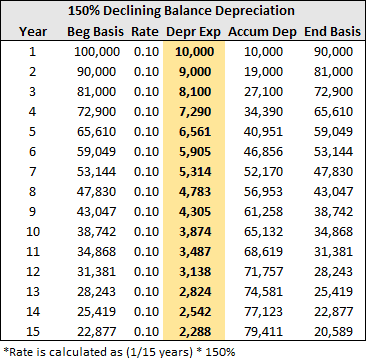

Straight line depreciation is the most straightforward method for calculating a new roof s depreciation.

Improvements are depreciated using the straight line method which means that you must deduct the same amount every year over the useful life of the roof.

The bonus depreciation percentage for qualified property that a taxpayer acquired before sept.

The depreciation is the same for each year of the roof s useful life.

Insurance valuation methods can be confusing and difficult to determine based on your individual needs and circumstances.

Once you know the start date calculating the depreciation is reasonably straightforward.

27 2017 and before jan.

The older the roof the more deducted for depreciation.

I entered the asset with the 39 year life and took the section 179.

Lacerte is giving me a critical diagnostic.

What are the irs rules concerning depreciation.

We replaced the roof with all new materials replaced all the gutters replaced all the windows and doors replaced the furnace and painted the property s exteriors.

The acv would be 15 000.

Your roof s depreciable life has been shortened by about 36.

1 2018 remains at.

The insurance company would take out the deductible and cut you.

Let s say it will take 20 000 to replace your roof and it was 5 years old and in good condition.

28 2017 and placed in service before jan.

First collect your receipts and calculate the total cost of the new roof.

The new law increases the bonus depreciation percentage from 50 percent to 100 percent for qualified property acquired and placed in service after sept.

See the tables above going from asphalt shingles 20 year life to clay tile 50 year life is a betterment because that would materially increase the capacity efficiency or quality of the building structure.

As you can see in the above example doe will receive 14 000 from his insurance company whereas smith will receive only 4 000.

Under the new rules for depreciation under the tax cuts and jobs act we can now take section 179 on nonresidential real property.

Invalid method for section 179 expense.

The acv is the amount it would take to replace your roof minus the depreciation calculated.

The new tax law shortens the commercial roof depreciation schedule from 39 years to 25 years that s an enormous difference.

The depreciation was 25 or 5 000.

We have incurred costs for substantial work on our residential rental property.

The irs uses the straight line method to calculate the depreciation of your roof which means that the depreciation of your roof is calculated evenly across a set period of time.