New Roof Depreciation 2019

Make The Most Of Your Section 179 Tax Deduction For Orthodontic Oral Surgery Pediatric Dental Endodontic And Mo Tax Deductions Business Tax Budgeting Money

179 Tax Deduction For Commercial Roofing Projects Advanced Roofing Inc

How To Understand Depreciation On Your Roof Insurance Claim

Section 179d Tax Deduction For Commercial Roof Replacements

Irs Issues Guidance For Change To Real Property Depreciation Grant Thornton

Confused With Tax Deductions In Recent Legislation Changes How You Claim Depreciation On An Investment Investment Property Stroud Homes Build Your Dream Home

1 2018 remains at.

New roof depreciation 2019.

Property Tax Get The Tricks For Lowering The Bill Property Tax Tax Consulting Indiana Real Estate

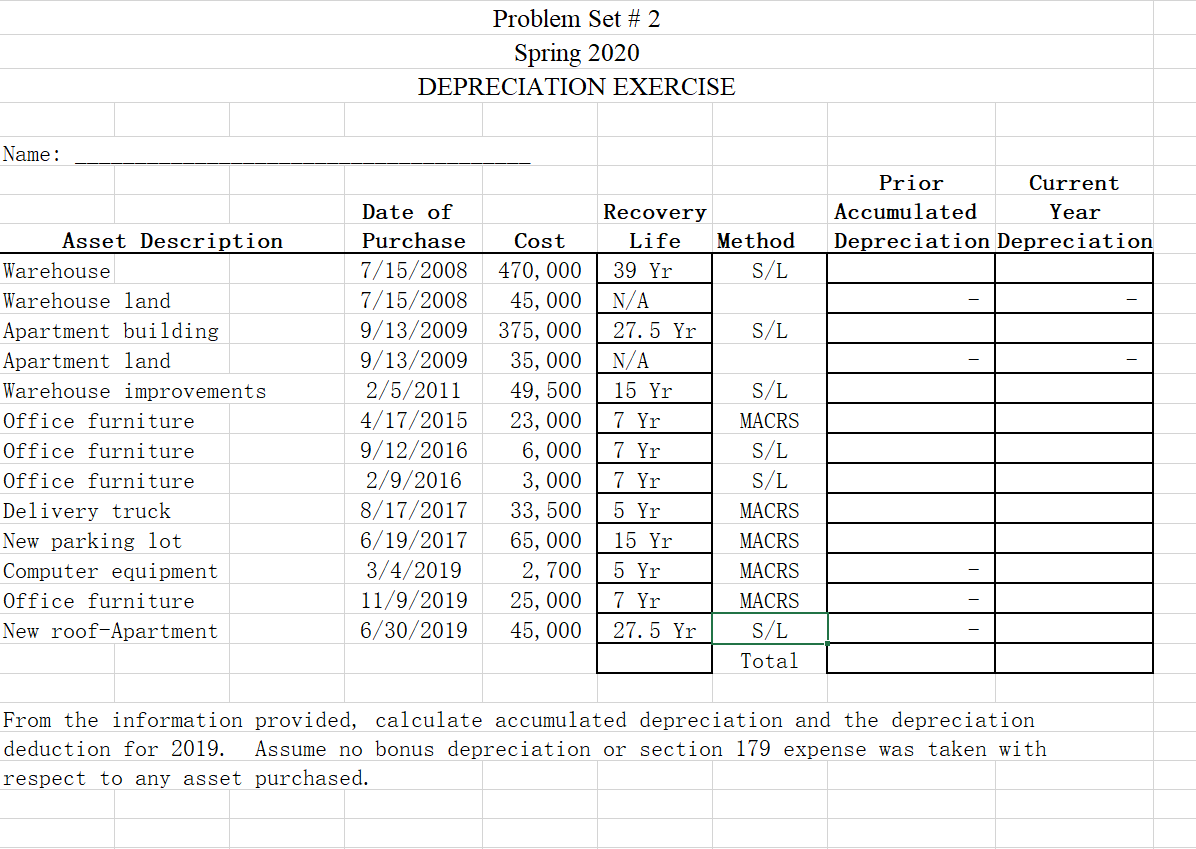

Problem Set 2 Spring 2020 Depreciation Exercise Chegg Com

Qquick To Answer Questions Good Work Easy To Communicate With The Finished Product Just What I Was Looking For Su Flyer Design This Or That Questions Flyer

Tcja Expands Section 179 Expensing Strategies Csh

Source : pinterest.com